The 2026 GST Roadmap for Nagpur Real Estate — Under-Construction vs. Ready-to-Move

As of March 25, 2026, GST remains one of the largest and most misunderstood extra costs for home buyers in Nagpur. The key rule is simple: GST applies to construction services, not completed immovable property. Understanding this distinction can directly save lakhs in total acquisition cost.

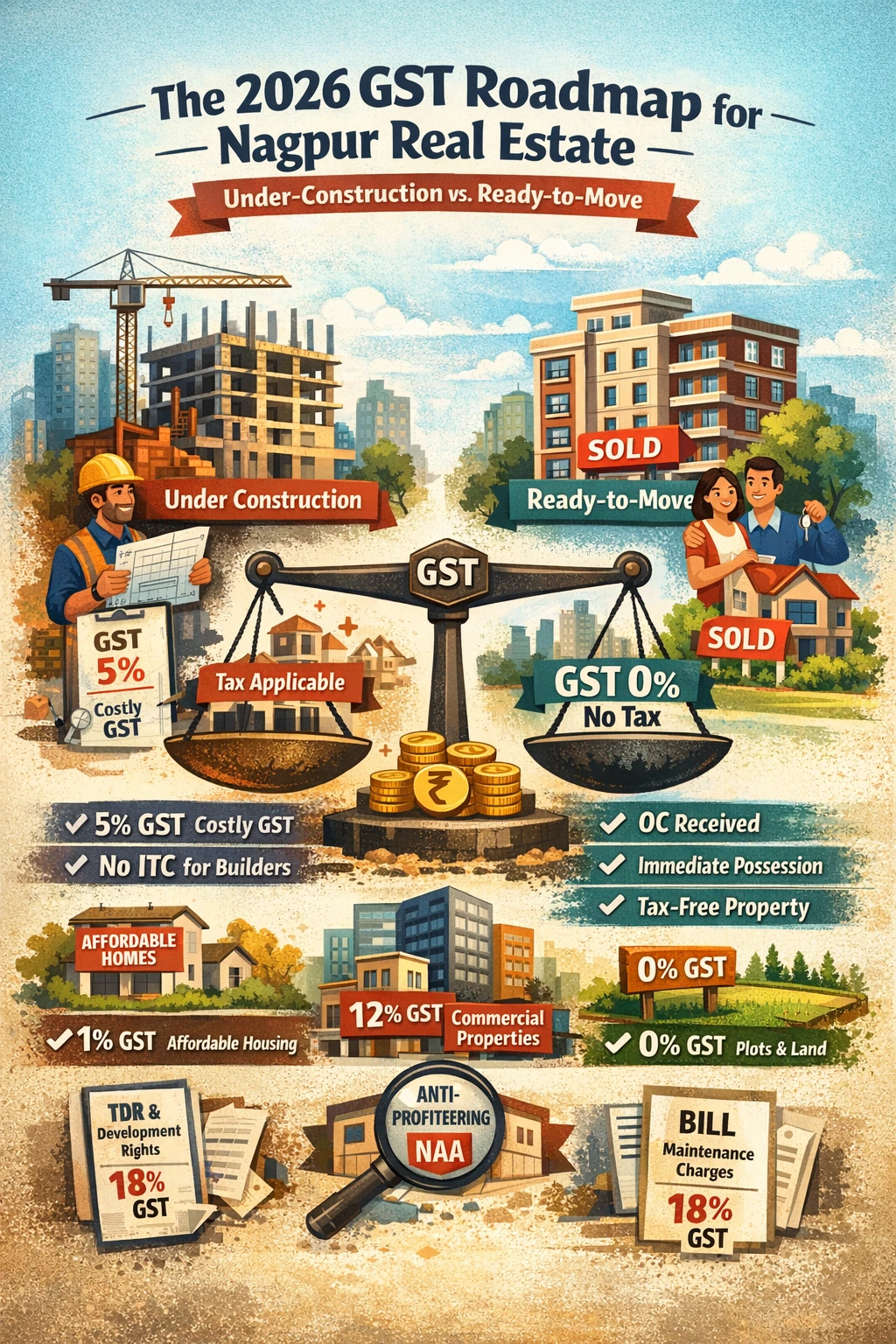

In 2026, choosing between under-construction and OC-received inventory is not just a lifestyle decision, it is a major tax decision.

The 2026 GST Framework

The current framework treats GST as a tax on construction services. So long as a project is under construction, tax applies. Once the project receives an Occupancy Certificate from NMC or NMRDA, the service is deemed complete and the unit becomes immovable property, where GST falls to 0%. For many buyers in markets like Manish Nagar, selecting OC-received inventory can mean savings in the range of ₹3 lakh to ₹8 lakh, depending on ticket size.

Under Construction

GST applicable because construction service is still being rendered.

Ready-To-Move (OC)

GST is 0% once valid occupancy certificate is issued.

The 5% Standard Rate

In most high-rise projects across Shankarpur, Wardha Road, and similar growth belts, the default residential GST rate is 5% without Input Tax Credit. This applies to non-affordable housing. In 2026 terms, a property falls into non-affordable if carpet area exceeds prescribed limits or value exceeds ₹45 lakh. Because many premium 2BHK and 3BHK units in Nagpur now cross that threshold, 5% has effectively become the benchmark rate in practice.

Affordable Housing & The 1% Advantage

Affordable housing enjoys a sharp tax subsidy. If the property value is below ₹45 lakh and carpet area remains within applicable limits, GST is only 1%. This is highly relevant in peripheral pockets like Wadi and Hingna. Buyers often optimize budgets around this cut-off because crossing ₹45 lakh by even a small amount can shift total tax from a manageable figure to several lakhs, changing affordability instantly.

The "No-ITC" Reality for Developers

Post-2019 reforms, residential developers cannot claim input tax credit in the usual way for these residential outputs. While this simplified visible tax rates for buyers, it also caused indirect base-price adjustments because taxes on inputs still flow through project costing. This is why "GST-inclusive" offers should be read carefully. In many cases, the tax is simply embedded in the quoted base rate rather than eliminated.

"Always evaluate total landed cost, not just advertised base price. In Nagpur 2026, tax structuring can change your real acquisition cost by several lakhs."

GST on Commercial Properties (12%)

Commercial units such as shops and offices typically attract 12% GST. The treatment differs from residential: input credit mechanisms are more usable in commercial chains, and businesses with valid GST registration may be able to claim credit against output liabilities based on use and compliance. For active business owners, this can materially improve effective acquisition economics over time when structured correctly.

Development Rights and TDR

In redevelopment-heavy locations like Dhantoli and Ramdaspeth, GST can also arise around development rights and Transferable Development Rights transactions. While developers usually handle these obligations, unresolved liabilities can ripple into project timelines and buyer risk. In 2026, buyers should ask for clear confirmations that such tax components are settled before final documentation and deed execution.

Land & Plotted Developments (0% GST)

For plots, the position is materially lighter. Sale of land does not attract GST under current clarifications, even when accompanied by basic site-level development such as leveling or internal roads. That means buyers in plotted zones like Yerla generally face stamp duty and registration, but not GST. This is one major reason land remains a preferred tax-efficient allocation for many high-net-worth investors in Nagpur.

GST on Maintenance Charges

GST exposure can continue post-possession through maintenance structures. Where monthly maintenance exceeds prescribed limits and society-level conditions trigger applicability, GST at 18% may apply. In premium Besa and Wardha Road communities with high-end amenities, this can be relevant to long-term ownership cost planning. Buyers should include this recurring tax impact while evaluating net monthly outgo.

The Anti-Profiteering Shield

Buyers should remain vigilant about anti-profiteering protections. If any tax benefit is legally available but not passed through, that can become a compliance issue. The practical safeguard is documentation discipline: insist on formal tax invoices for every installment. These records protect buyers during registration, future scrutiny, and any dispute around tax treatment or builder-side pass-through claims.

The Property Bhandar Guidance

At Property Bhandar, our GST-first advisory helps you compare under-construction, ready-to-move, commercial, and plotted options on actual post-tax cost, not headline pricing. Before finalizing any deal in 2026, use our verification checklist to confirm OC status, tax slab eligibility, invoice trail, and total ownership outgo so your purchase is legally clean and financially optimized.

Get GST Verification Support